Taxation

Taxation

Level: AS Levels, A Level, GCSE – Exam Boards: Edexcel, AQA, OCR, WJEC, IB, Eduqas – Economics Revision Notes

The main aims of Taxation

- To raise revenue for public expenditure

- A way to manage the part of the economy – fiscal policy

- To redistribute income

- To correct market failure

- To internalise external costs

- To improve incentives

- Defence and internal security

Progressive, Regressive, and Proportional Taxes

Progressive Taxes

As income rises, so does the amount of tax paid back to the Government. Income Tax tends to be progressive as it is an example of a direct tax

Examples of countries with a Progressive Tax System: UK, China

Regressive Tax

As income rises, the amount of tax paid decreases. Those on lower incomes pay a higher percentage of their income on tax.

Examples of countries with a Regressive Tax System: Norway, Switzerland, Netherlands, Denmark

Proportional Tax

The amount of tax paid from income remains the same regardless of a change in income generated

Examples of Countries with a Proportional Tax System: Bulgaria, Hungary, Bolivia

The Impacts of Tax Changes

Incentives to work

- Individuals may be discouraged from working if they are forced to pay huge amounts in tax

- Free Economists argue that the supply of labour tends to be relatively elastic and a reduction in marginal taxes on income will lead to a larger supply of workers

- Poverty Trap – taxes on the poor may result a poverty trap due to the downward spiral caused

- Individuals may be demotivated to work in the country – if high income earner are forced to pay a large amount in tax, they may choose to move aboard to countries where the tax rates are lower

Income Distribution

- A Progressive Tax System aims to reduce the income inequality between the rich and poor as the rich are taxed with more and the poor are taxed with less

- A Regressive Tax System will increase the income inequality between the rich and poor

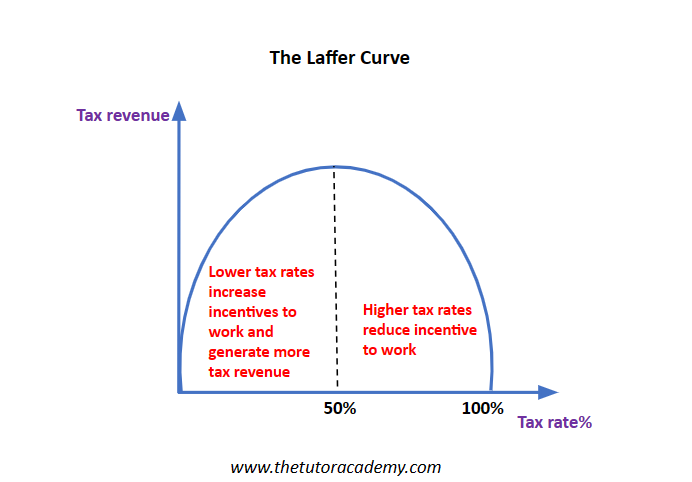

Tax Revenues

- With the use of a Laffer Curve, a rise in tax does not necessarily mean tax revenue will rise – if individuals are taxed at an excessively high rate, they may lose motivation to work and will instead end up paying less tax

- M depicts the optimal level of tax which will generate the most amount of tax revenue

Real Output and Employment

- AD – direct taxes affect the level of AD. For e.g. a rise in direct taxes will reduce the level of disposable income an individual has, resulting in a decrease of aggregate demand. There may also be a loss of output if businesses choose to invest less

- SRAS – higher indirect taxes may increase the costs that firms endure and hence cause a decrease in the SRAS curve

- LRAS – higher income taxes may cause a disincentive to work and a loss of skilled workers, reducing LRAS

Price Level

- Since taxes can impact AD, SRAS, and LRAS, the price level in the economy will also be affected

FDI

- Higher levels of FDI – If companies are faced with lower taxes, they will have more income available for investment. Therefore, businesses are likely to invest in other countries as they can receive a higher level of return

- Loss in Tax Revenue – Although countries with the lowest tax rates will attract the most investment, in the long-run, they experience a loss in tax revenue generated

Trade Balance

- Less Imports – Higher taxes will leave households with less income, hence they will be encouraged to save their money instead of spend. Less consumption means that individuals spend less on imports

- Improve Trade Balance – In the UK, imports tend to be highly income elastic which may improve the trade balance in the short-run

- Reduce Competitiveness – In the long-run, lower AD will discourage businesses to invest, leading to less competitiveness and a decrease in exports

CIE Spec – Additional Content

The Canons of Taxation

These refer to the criteria taxes are assessed by. They were developed by Adam Smith and include:

- In comparison to the yield, the cost of collecting the tax must be low

- The tax payer must be aware of the timing and quantity paid

- The timing and method of payment should be convenient for the tax payer

- Taxes should be imposed depending on the ability to pay

- There should only be a minimum loss of efficiency – the tax should not limit efficiency

- The tax should be compatible with tax systems in other countries

- Taxes should be able to adjust to differing levels of inflation

Quick Fire Quiz – Knowledge Check

1. Identify five main aims of Taxation (5 marks)

2. Explain the difference between a Progressive, Regressive, and Proportional Tax System (6 marks)

3. Identify and explain the impact of Tax Changes on the Incentives to Work (6 marks)

4. Identify and explain the impact of Tax Changes on the Income Distribution (4 marks)

5. With the use of a Laffer Curve, explain the impact of Tax Changes on Tax Revenues (6 marks)

6. Identify and explain the impact of Tax Changes on the Real Output and Employment (6 marks)

7. Explain the impact of Tax Changes on the Price Level (2 marks)

8. Identify and explain the impact of Tax Changes on the FDI (4 marks)

9. Identify and explain the impact of Tax Changes on the Trade Balance (6 marks)

Next Revision Topics

- Public Expenditure

- Public Sector Finances

- Macroeconomic Policies in a Global Context

A Level Economics Past Papers