Costs

Costs

Level: AS Levels, A Level, GCSE – Exam Boards: Edexcel, AQA, OCR, WJEC, IB, Eduqas – Economics Revision Notes

Costs in the Short Run

Total Costs – calculated by adding the total fixed costs and the total variable costs

Fixed Costs – costs which do not vary with output. They can also be called ‘Overheads’ and examples of these include rent, insurance, loan repayments

Variable Costs – costs which do vary with output and can also be known as ‘Direct Costs’. Examples of these include raw materials, delivery costs, commissions

Average Costs

- These are the total costs divided by the quantity produced

Average Fixed Costs – the fixed cost which remains the same regardless a change in the goods / services being produced

Average Variable Costs – the variable cost per unit of total output produced

Marginal Cost – the cost of producing one extra unit of output. They are derived from variable costs and are not affected by changes in the fixed costs

Short-Run Cost Curves

[diagram]

- Cost curves in the short turn tend to possess a U shape due to the Diminishing Returns theory

- Diminishing Returns – only applicable in the short run and when at least one factor of production is fixed. As more variable factors are added to the fixed factor, the increase in output will eventually fall

- Marginal Product – the additional output produced when one more factor of production is added

- Fixed Factor – the factor of production which cannot be changed in the short run

- Marginal Cost curve possess a ‘tick’ shape which suggests that initially it may fall but then at some point it will start to rise and continue to do so. The MC curve goes through the lowest point on the Average Total Cost Curve

- When Marginal Cost < Average Variable Costs, the cost of producing an additional unit is less than the current average cost of producing. This extra unit of output will reduce the average cost, but it will not fall as much as the marginal cost. When MC is above ATC, ATC will be rising.

- A firm is most productively efficient when Average Total Cost = Marginal Cost

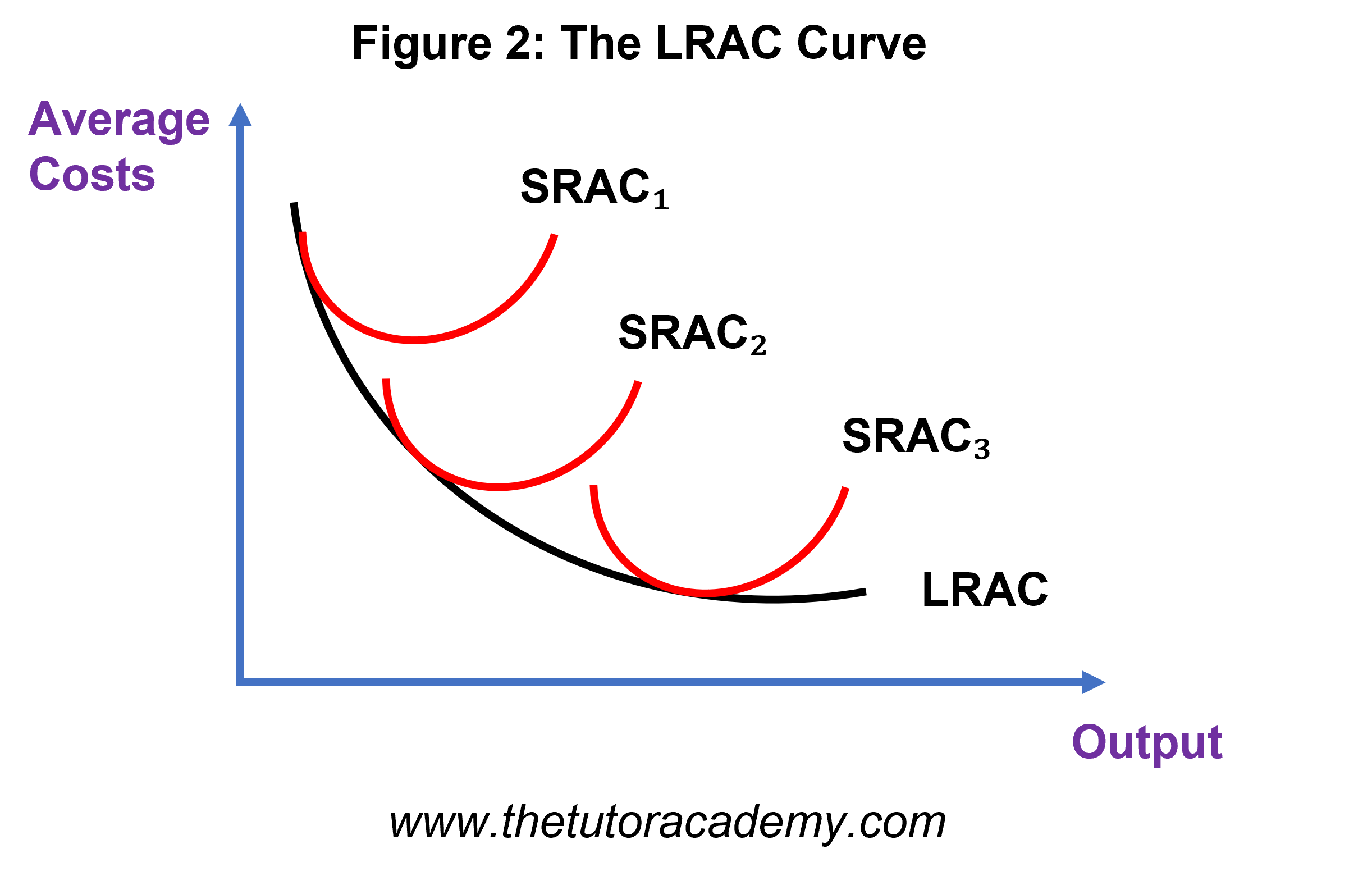

Costs in the Long Run

- In the long run, there are no fixed costs – all the costs are variable

- Economies of Scale – when the average costs per unit of output fall as the scale of output being produced rises in the long run

- Diseconomies of Scale – when the average costs per unit increases with the output being produced

Economies of Scale (Internal)

- Financial Economies – larger firms have can access a wider range of credit at a lower price than smaller firms; they can also issue shares on the stock market and make deals with lenders where they are able to borrow money at a cheaper rate

- Managerial Economies – larger firms can afford better managers or a better management system which will lead to higher profits and sustainability

- Technical Economies – larger firms possess the ability to invest more into better technology and also have more capital available. Processes can be easily scaled up to produce a much larger volume of goods / services

- Commericial Economies – larger firms can bulk-buy from their suppliers where they are able to purchase a large amount of goods for a cheaper price in comparison to smaller firms

- Risk-bearing Economies – larger firms are able to bear business risks more effectively than smaller firms

Economies of Scale (External)

- Cluster Effect – it becomes more efficient for suppliers to meet a larger base of purchases if firms locate in similar areas

- Transport Links – new firms can enter a market or existing ones can expand and take advantage of infrastructure already built to get lower average costs. Mining can also help improve the transport links for shipping goods into the market

- Skilled Labour – if similar firms locate to a specific region, it can encourage skilled worker to seek employment in this area and firms may incur a more time-effective recruitment process

Diseconomies of Scale

- Managerial Diseconomies – large firms are likely to have more than one manager in place which may cause diseconomies of scale if the management system weakens as a result of conflict between the managers or poor coordination

- Communication – workers in a large firm may experience delays if there is a lack of communication between colleagues or if they are waiting for someone else to finish their tasks so that they can complete theirs

- X-inefficiency – larger firms may operate in uncompetitive markets which lead to higher costs and more waste products being produced

- Slowness – larger firms may experience slow decision-making if they need approval from a majority of senior members

Minimum Efficient Scale

- Concept which applies to firms with high fixed costs

- MES occurs at the point where average costs are kept at the minimum

AQA Spec – Additional Content

How factor prices and productivity affect firms’ cost of production and their choice of factor inputs

More productive factor inputs – firms can produce more output with less factor inputs if they become more productive, leading to lower unit costs of production

Increase in cost of factor inputs – if the average cost per unit of factor inputs increase, firms will most likely switch to cheaper alternatives

Quick Fire Questions

1. Define ‘Total Costs’ (2 marks)

2. Distinguish between ‘Fixed Costs’ and ‘Variable Costs’ (4 marks)

3. Explain the difference between ‘Average Fixed Costs’ and ‘Average Variable Costs’ (4 marks)

4. Define ‘Marginal Cost’ (2 marks)

5. Draw Short Run cost diagram, labelling the ATC, AFC, AVC, and MC (4 marks)

6. Using the diagram, explain what shapes each of the short run cost curves possess and the reasoning behind this (6 marks)

7. Distinguish between ‘Economies of Scale’ and ‘Diseconomies of Scale’ (4 marks)

8. Identify and explain five Internal Economies of Scale (10 marks)

9. Identify and explain three External Economies of Scale (6 marks)

10. Identify and explain four Internal Diseconomies of Scale (8 marks)

11. Using a diagram, explain what is meant by the ‘Minimum Efficient Scale’ (4 marks)

Next Revision Topics

- Economies of Scale

- Diseconomies of Scale

- Revenue

- Profit

- Business Objectives

- Business Growth

- Size and Types of Firms

- Efficiency

- Factors of Production

A Level Economics Past Papers